Most of us know the basics.

Save consistently.

Don’t overspend.

Avoid unnecessary debt.

Invest for the long term.

The information is everywhere. Books, podcasts, finance influencers, economics classes — we are not short on advice.

And yet, we still impulse buy.

We procrastinate investing.

We hold losing stocks.

We swipe cards we shouldn’t.

The problem isn’t ignorance.

It’s that humans aren’t rational calculators — we’re emotional decision-makers trying to look rational afterward.

The Myth of the Rational Human

Traditional economics assumes something called Homo economicus — a person who weighs costs and benefits logically and consistently.

In reality, we:

- overestimate future self-control

- underestimate future expenses

- overreact to losses

- chase short-term pleasure

We don’t optimize. We justify.

And that gap between what we know and what we do is where behavioural economics begins.

Reviewing ‘Predictably Irrational’ by Daniel Ariely

In his book Predictably Irrational, behavioral economist Daniel Ariely argues something deeply unsettling:

We aren’t randomly irrational.

We are predictably irrational.

Our mistakes follow patterns.

Ariely shows how people:

- value things more once they own them (endowment effect)

- anchor decisions around irrelevant numbers

- overspend when using credit instead of cash

- choose “free” options irrationally

One of his famous insights is that pricing and framing change behavior more than logic does. If something is labeled “free,” we lose all sense of proportional judgment. If a high price is shown first, everything else looks reasonable by comparison.

These aren’t rare glitches. They’re systematic.

And that’s exactly why we’re bad with money — even when we understand the math.

We don’t experience money objectively.

We experience it psychologically.

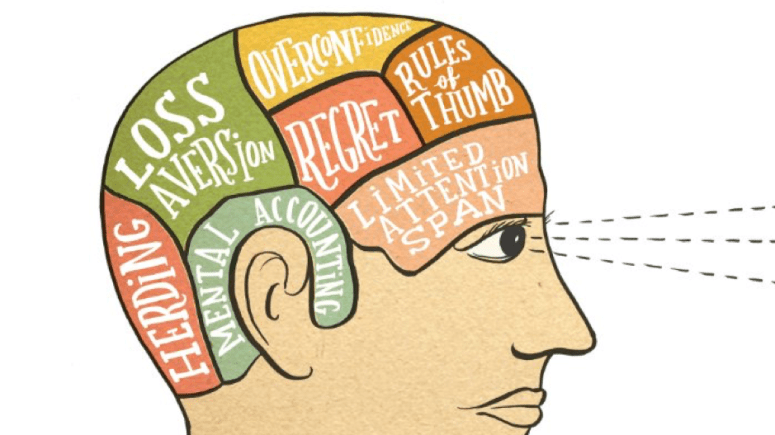

Mental Accounting: Why Money Isn’t Just Money

Logically, ₹1,000 is ₹1,000 — no matter where it comes from.

But in our minds, money sits in separate mental boxes.

Tax refunds feel like “bonus” money.

Salary feels serious.

Cash feels limited.

Credit feels abstract.

We spend differently depending on which “account” money comes from — even though economically, it’s identical.

This is why people splurge windfalls but hesitate to touch savings. It’s not about numbers. It’s about labels.

Loss Aversion: Why Losing Hurts More Than Winning Feels Good

One of the most powerful behavioural insights is loss aversion.

We feel losses about twice as intensely as equivalent gains.

So:

- We hold losing investments too long.

- We refuse to sell assets at a loss.

- We avoid risks even when the expected payoff is positive.

We aren’t just bad at calculating probabilities — we’re emotionally allergic to loss.

And markets know this.

Present Bias: Why Future Us Is Always Richer

We tell ourselves:

“I’ll start saving next month.”

“I’ll invest when I earn more.”

“I’ll budget once things calm down.”

Present bias makes current consumption feel more urgent than future stability. We discount the future too heavily.

Future us always seems:

- more disciplined

- higher earning

- more responsible

But when the future arrives, it becomes the present — and the cycle repeats.

Why This Isn’t Just Personal; It’s Also Structural

Our financial systems are built in ways that exploit predictable irrationality.

Easy credit reduces the “pain of paying.”

Buy-now-pay-later models separate consumption from consequence.

Subscription services rely on inertia.

Companies understand behavioral biases deeply. Consumers often don’t.

This doesn’t mean we’re foolish. It means we’re human in systems optimised for our weaknesses.

So What Do We Do?

If we’re predictably irrational, the solution isn’t to “try harder.” It’s to design systems that protect us from ourselves.

Automatic savings.

Default retirement contributions.

Spending limits.

Cooling-off periods before large purchases.

Behavioural economics doesn’t aim to shame us. It aims to nudge us toward better outcomes by acknowledging how we actually behave.

Because the problem was never that we lacked information.

The problem is that knowing something isn’t the same as feeling it.

The Real Lesson

We’re bad with money not because we’re careless — but because money triggers emotion, identity, fear, and desire all at once.

Economics once assumed we were rational.

Behavioural economics showed we are predictably human.

And maybe that’s comforting.

You’re not financially flawed.

You’re just operating with a brain designed for survival — not spreadsheets.

Leave a comment